UOB definitely got everyone’s attention with the recent introduction of an elevated interest savings account plan. The UOB ONE Account is a pretty attractive plan on paper with a maximum possible saving interest rate “up to” 3.33%, the highest offered by any bank in Singapore to date. Standard Charted first started this with their bonus saver accounts, which are not as popular as the OCBC 360, which had proven that the best method for banks to rake in massive cash in-flow in the shortest time possible.

UOB had always known for their attractive fixed despots (FDs), but this latest offering will possibly kill off FDs altogether today. The UOB One Account looks to offer two different plans with two fixed maximum interest rates at 2% p.a. and 3.33% p.a., based on your contributions to your savings account (up to $50,000), with the latter beginning the more feasible one. The catch is that you do not get the full 3.33% p.a. interest rate up front from your minimum deposit, but rather only from your $30,001-th dollar. UOB also requires a minimum salary contribution of S$2,000, 3 GIRO deductions and S$500 minimum credit card spend on a UOB One Card- really similar to OCBC 360 offerings.

A quick summary and comparison of both banks offerings and your return of investment from various deposit amounts ($20k-$50k) in the table below:

|

Plan/Bank

|

UOB One Account (3.33% tier)

(Min deposit $2000) |

OCBC 360

(Min deposit $1000) |

|||||

| Annual $ interest earned | Annual $ interest earned | ||||||

| Constituent item | Interest Rates | E.g. $20k deposit | E.g. $40k deposit | E.g. $50k deposit | Interest Rate | E.g. $20k deposit | E.g. $50k deposit |

| Savings | 1st $10k: 1.5% Next $20k: 2.0% Next $20k: 3.33% Above $50k: 0.05% (basic rate) |

$150+ $200 | $150+ $400+ $333 | $150+ $400+ $666 | Determined by constituent items | ||

| Monthly salary credit (min. S$2,000) | 1.2% Up to $60k | $240 | $600 | ||||

| GIRO credit | 0.5% | $100 | $250 | ||||

| Credit card spend (min $500) | 0.5% | $100 | $250 | ||||

| Save bonus (e.g. $1000) |

NA

|

NA

|

NA

|

NA

|

1% | $10 | $10 |

| Total yearly (monthly) |

–

|

$350.00 ($29.17) |

$883 ($75.58) |

$1216.00 ($101.33) |

–

|

$440.00 ($36.67) | $1100.00 ($91.67) |

| Annual ROI |

–

|

1.75% | 2.21% | 2.43% |

–

|

2.20% | 2.20% |

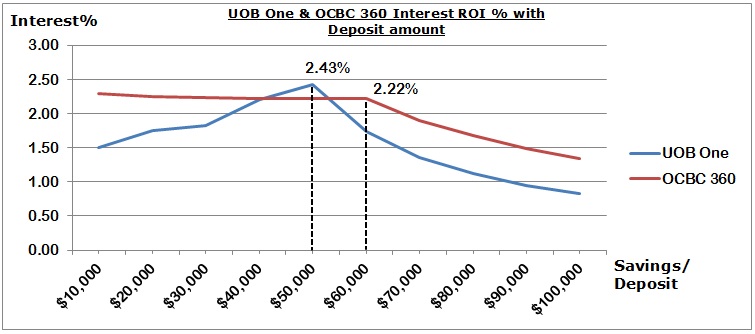

To grasp a better understanding of the interest rate sensitivity between the two banks offering, when you plot the p.a. interest ROI to savings/deposit (e.g. $10,000 to $100,000), you will notice the OCBC tend to favour small deposits, with near-constant interest rates from the $3,000 minimum amount, while the UOC plan has a linear increasing interest rate peaking at a maximum nominalised value of 2.43% p.a. (and not as the collective “3.3%” as claimed) which is overall higher than OCBC offerings.

Once past the $60,000 mark, your money is working much lesser for you, with the ROI from both banks falling drastically below the 2% mark. UOB offerings are on average 0.5% lower than OCBC’s per dollar, as such it is not recommend to leave any amount beyond $60k with UOB.

Assumptions of analysis:

- Calculated based on a monthly $1,000 savings (for OCBC saving interest), which is representative of an “average savings rate”, though this adds a somewhat negligible 0.01-0.02% p.a. to OCBC p.a rates.

- Excludes the respective credit cards rebate perks.

- Excludes additional interest from investment and insurance packages, which is not relevant for most customers on these plans.

With that, I have recommendations from 3 possible scenarios:

- You have the option to open an account with either bank.

If you have under $40,000, go for OCBC 360, as the entry interest rate is consistent starting from the minimum deposit sum. At $40,000 deposit, the savings ROI is similar for both banks. However, if wish to obtain the maximum possible interest rate from your savings and have at least $50,000, go for UOB One, you will earn $105 more p.a. (at $50,000) than the OCBC 360. - You are currently on OCBC 360.

Stick to OCBC 360, as the interest rate difference between the two is somewhat too low to be worth the hassle for a switch. (Maximum interest difference is 0.21% or $105 p.a. from $50,000 savings). - You have over $100,000 in saving deposits.

It is recommended to split your pie between both banks which each account not exceeding $60,000 each. If you are currently with OCBC and maxed out your 360 account $60,000 bonus interest cap, opening an alternative account with UOB and putting at least $50,000 will bring you the best of both worlds, topping with a savings ROI of ~4.65% collectively. It is not recommended to leave over $60,000 in either account given opportunity costs of investing it elsewhere (e.g. the Singapore government bonds for instance).

Hope this analysis helps, if you have any queries or doubts of my evaluation methodologies; do feel free to open it for discussion at the comments below.

{kind=link}

Excellent article! We are linking to this particularly great article on our website. Keep up the good writing.

This is really cool info!

Very shortly this web page will be famous among all blog viewers, due to it’s pleasant articles

Spot on with this write-up, I truly believe this amazing site needs a lot more attention. I’ll probably be back again to read more, thanks for the information!

Hi there, You have performed a fantastic job. I’ll definitely digg it and in my view suggest to my friends. I am sure they will be benefited from this website.

[…] interest rate cut). This includes UOB One Account for UOB, OCBC 360 and DBS Multiplier which I touched on a couple of years back. Let’s take a look at how drastic the cuts are and which is the best to go […]